When we talk about Amazon (AMZN), it is mostly about the product that we saw or ordered and whether they were decent or a waste of money. The retail business made Amazon an e-commerce giant, rewarding investors with gains of more than 15,700% over the last 20 years. Many still see Amazon as the website or app where they can simply order things. Very few may have noticed that Amazon has quietly transformed into a tech and artificial intelligence (AI) powerhouse that is becoming a full-stack AI infrastructure empire.

It may not be entirely correct to say that the Amazon investors knew it doesn’t exist anymore. Retail and e-commerce are still deeply embedded in the company’s core business. However, while retail made Amazon, AI and technology are building its future.

And its Q1 earnings reveal just how huge this transformation has become. Let’s dig in deeper.

Amazon’s Retail Business Is Still Going Good, but It Is No Longer the Whole Story

Amazon reported first-quarter revenue of $181.5 billion, up 17% year-over-year (YoY), while adjusted earnings rose 75% to $2.80 per share. Its retail business still continues to expand rapidly, with unit growth of 15% YoY, which marked the highest level since the later stages of Covid-19 lockdowns. Amazon also added more than 600 notable new brands during the quarter. Its grocery business exceeded $150 billion in gross sales in 2025, making it the second-largest grocer in the U.S.

CEO Andrew Jassy made it clear that Amazon now sees itself at the center of one of the largest technology shifts in decades. According to him, the company has “never seen a technology grow as rapidly as AI.” AI is now embedded across Amazon’s entire business, driving a 28% YoY increase in its cloud computing business, AWS. Management said AWS’s AI business has already reached a revenue run rate of more than $15 billion within just three years of the current AI boom, making it nearly 260 times larger than AWS’s cloud business was in its early years.

Amazon Is Becoming an AI Infrastructure Empire

What separates Amazon from other tech companies is that it is not just building AI applications. It is, in fact, trying to control every layer of the AI infrastructure stack. Its AI ecosystem now includes model-building tools through SageMaker, AI inference services, frontier AI models on Bedrock, enterprise AI agents, custom AI chips, data center infrastructure, cloud computing services, and agentic AI platforms.

Amazon Bedrock has become one of the company’s most important AI products, with nearly 80% of Fortune 100 companies using it. Its biggest weapon might be chips. While most investors associate AI chips with Nvidia (NVDA), Amazon revealed that its "custom silicon business is now one of the top three data center chip businesses in the world." Its chip business grew nearly 40% sequentially during Q1, with an annual revenue run rate now exceeding $20 billion and growing at triple-digit percentages YoY. Amazon also stated that if its chip business operated independently and sold chips externally like traditional semiconductor companies, its annual revenue run rate would already be approximately $50 billion.

Its Trainium AI chips are becoming important to its AI strategy, with over $225 billion in revenue commitments tied to Trainium. The company revealed that Trainium3, which started shipping in 2026, has already seen nearly all of its capacity booked by customers. Meanwhile, Trainium4, which is still 18 months away from availability, has already been heavily reserved. Amazon has already secured multiyear, multi-gigawatt training commitments from both OpenAI and Anthropic, while companies like Uber (UBER) are increasingly adopting Trainium as well.

Amazon, like Intel (INTC), feels that AI is more than simply a GPU-driven opportunity. It is also dramatically increasing CPU demand. The company revealed that Meta alone has committed to using tens of millions of its Graviton CPUs for AI workloads. What’s more, its autonomous vehicle business, Zoox, has now driven nearly 2 million miles and transported more than 350,000 riders. Meanwhile, its satellite internet business, Amazon Leo, is almost ready for commercial launch. Delta Air Lines (DAL), JetBlue (JBLU), AT&T (T), Vodafone (VOD), NASA, and other large clients have already made commitments to the company.

The Amazon Investors Once Knew Is Evolving Into Something Much Bigger

Many investors continue to associate Amazon with retail. But these developments show that Amazon has expanded far beyond traditional retail. It is becoming a global AI infrastructure provider, a semiconductor company, a cloud giant, an advertising platform, a healthcare technology business, a logistics network, a robotics operator, a satellite communications player, and an enterprise AI ecosystem all at the same time. And these could shape what Amazon will become in the next decade.

With such a diversified business, I believe AMZN is an excellent buy-and-hold stock for the long haul.

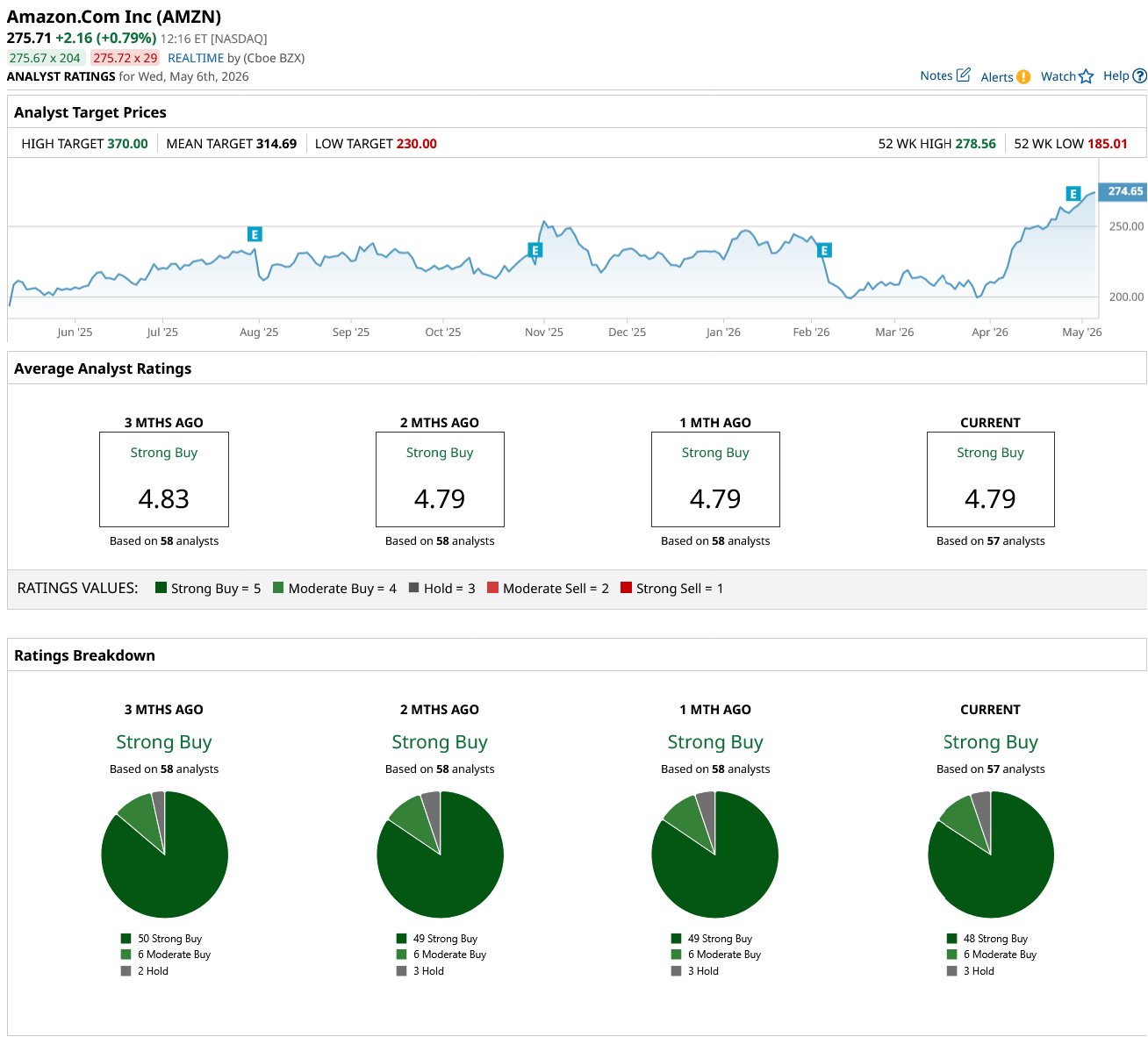

Overall, on Wall Street, AMZN stock has earned a consensus “Strong Buy.” Of the 57 analysts covering the stock, 48 have a “Strong Buy,” six have a "Moderate Buy" rating, and three analysts rate the stock as a “Hold.” AMZN stock has climbed 18% year-to-date (YTD). But its mean target price of $314.69 implies 14% potential upside from current levels. Plus, the high target price of $370 suggests that shares could climb as much as 34% over the next year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- With Earnings Ahead, Wait for a Dip Before You Buy CoreWeave Stock

- Sandisk Stock Is up Nearly 500% in 2026. Q3 Results Show Its Data Center Business Is Still Growing.

- The Biggest Catalyst for OKLO Stock May Not Be Earnings, But a Brewing Short Squeeze

- 7 Stocks Worth Buying the Dip in Now... Or At Least Adding to Your Watchlist